Categories

NEWS: Are Mortgage Rates Going Down? [April 2026]

No, mortgage rates are not currently going down. For example, average 2-year fixed rate deals saw a sharp rise in the spring, rising from 4.83% in February to reach highs of 5.90%. In late April, this has dropped slightly to 5.79%, but there is no guarantee that rates will continue to ease.

Here’s a snapshot of the best mortgage rates on the market currently (updated live), so you can see how the lowest rates are shaping up:

So what does this mean for mortgage rates and affordability going forward?

In this post, we provide expert insight into the latest thoughts from our mortgage brokers, along with insight into what mortgage rates will do next, and how a decrease in mortgage rates could affect your repayments.

Get a Free Quote Today

Table of Contents

What Do Our Experts Say?

George Abouzolof

Senior Finance Broker CeMAP

In April 2026, the Bank of England has decided to hold the base rate at 3.75%, following a drop from 4.00% in late 2025.

A further drop to 3.5% had previously been expected to come in the early months of 2026, however the outbreak of the war on Iran has had a significant impact on global energy markets. As a result, rate setters have decided to act more cautiously.

Borrowers are unlikely to see big changes in mortgage rates in the short term, but the Bank of England's stance is to ensure stability in the UK market through 2026, which will likely ease borrowing rates in the longer term.

What Has Caused Mortgage Rates to Rise Recently?

Mortgage rates in the UK have risen sharply over the last month due to a combination of heightened geopolitical tensions, renewed inflation, and shifting expectations regarding the Bank of England’s interest rate decisions over the rest of 2026.

The sharp uptick so far in April 2026 has reversed a previous trend of falling rates, driven primarily by concerns that the war on Iran will continue to damage the economy and keep inflation higher for longer.

Here are the key factors causing mortgage rates to rise as of April 2026:

- War on Iran and energy costs: The escalation of war on Iran, resulting in blockades on the Strait of Hormuz, has caused oil and gas prices to spike. As a major energy importer, the UK faces higher inflation (3.3% in March 2026, up from 3% in February) as businesses pass on these increased energy and transport costs

- Higher-than-expected base rates: Prior to the outbreak of conflict, markets expected the Bank of England to continue cutting interest rates in early 2026. However, the threat of renewed inflation driven by rising oil and gas prices has forced a re-evaluation

- Rising swap rates: Fixed-rate mortgages are priced based on the cost lenders pay to secure funding. This is known as swap rates. These swap rates sharply increased in response to the war on Iran, prompting lenders to raise their fixed deals

- Reduced market competition: Lenders responded to the sudden market changes following the outbreak of war in Iran by pulling hundreds of products. This has reduced competition, while lenders simultaneously increased rates on fixed-term products

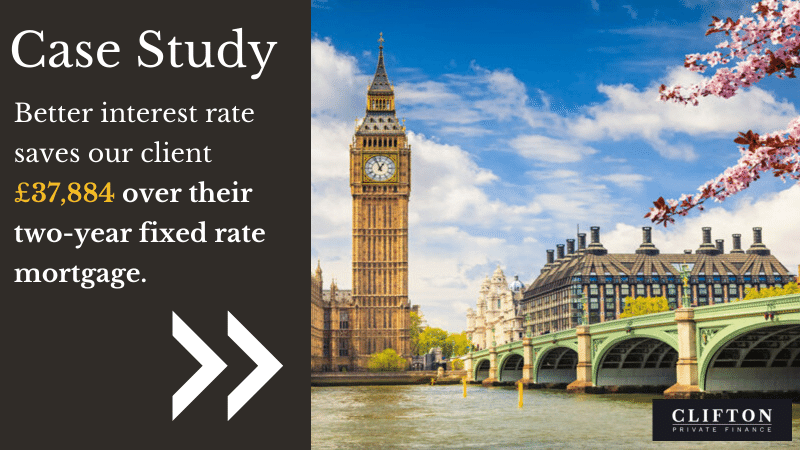

Case Study: Read our case study below of how we helped our client save thousands of pounds on their mortgage deal.

How Is the Mortgage Market Affected by Interest Rate Changes?

Tracker mortgages and standard variable rate (SVR) mortgages are both directly influenced by the Bank of England's base rate, while fixed rate products are also heavily affected.

- Tracker mortgages: These products directly track the base rate, so if the Bank of England increases the base rate by 0.25%, your mortgage rate also increase by the same percentage

- SVR mortgages: Lenders adjust their rates on these products as a result of base rate changes, but they are not directly tied, so the changes in rate may not match the exact base rate change

- Fixed-rate mortgages: Changes in the base rate will not affect your repayments if you have already fixed, but the base rate has a significant impact on swap rates, which lenders use to set new fixed rate deals - so higher base rates means higher fixed rate deals on the market when renewing

The Bank of England has voted to hold the base rate at 3.75% on 30th April 2026.

This move is aimed at supporting economic stability and encouraging growth across the UK. Over the past 12 months, the Bank’s approach has been to steadily reduce the base rate in response to inflationary pressures and the broader cost of living crisis.

Economic recovery has been slow but steady: the UK economy grew by 1.4% in 2025 following a small growth in 2024. However, this is expected to slow over the course of 2026.

Earlier in the year, many experts predicted that the Bank of England would continue to lower the base rate. But the outbreak of the war on Iran and the impact it has had on global energy prices has created a volatile situation with no clear end in sight.

As a result, expectations have changed and it is very unlikely that the base rate will drop further any time soon.

How is the Property Market Affected By Interest Rates?

When interest rates rise, it becomes more expensive for consumers to borrow money. Naturally, this includes mortgages for would-be buyers. Higher interest rates have an impact on the property market in a number of ways:

- Lower demand: Higher interest rates can make mortgages less affordable for first time buyers, leading to lower demand for homes.

- Reduced affordability: Rising rates also affect second property buyers and buy-to-let investors. Their mortgage payments could go up, meaning they may need to raise rent to compensate. Or, their projected rent won't meet the affordability for a mortgage on a new investment property, so they don't buy, reducing demand.

What Mortgage Types Are Most Affected By Interest Rate Changes?

If you have a mortgage with a variable interest rate, you will have seen your mortgage costs go up since 2022-23.

However, if you're on a fixed-rate mortgage, you may still have a year or two remaining before you need to renew, depending on the length of your term. But you could still be stung when your deal ends and you do remortgage.

Currently, many homeowners are coming to the end of low fixed-rate deals that they secured in 2021-2023, and are waiting with bated breath in hopes that rates will drop before they need to remortgage on a new deal.

Monthly increases in mortgage payments have been more acute for those whose fixed-rate mortgages ended recently and they have automatically switched to their provider's SVR (standard variable rate), these are typically the most expensive interest rates to pay.

We always recommend speaking to an independent mortgage broker about your options at least 6-months before your existing fixed rate ends. This is to avoid moving onto an SVR.

Related: What is a Green Mortgage, and how do they work?

Are Mortgage Rates Going Down Now?

No, mortgage rates are not currently falling. Although there are signs that the market may be starting to ease a little.

The Bank of England's decision to hold the base rate at 3.75% shows that they are committed to encouraging stability in the UK market despite geopolitical pressures on the economy.

Fixed rates have risen over 5% again during the spring, with highs of 5.9% from some lenders, and there is no guarantee that significant reductions will come later in the year while the war on Iran continues to impact global markets.

Related: How bridging loans can help you plug a funding gap and secure your property.

What Do Higher Mortgage Rates Mean for First Time Buyers?

With less favourable mortgage rates available on the market, it is a challenging time to secure yourself an attractive fixed rate deal.

The best strategy is to consolidate your finances, understand your borrowing power, and seek a mortgage broker's help to find the best deal for your circumstances.

Case Study: Read our case study below on how we helped our client borrow 5.5 times their self employed income.

How Can You Find an Affordable Mortgage in 2026?

Despite current market impacts on mortgage rates, deciding on the best option is still possible if you are looking to secure a new home.

We can help you compare mortgage products and their cost to find the best deal based on your specific situation from a wide range of lenders nationwide.

Our mortgage experts have their finger on the pulse of the latest mortgage market news. Whether you're a first-time buyer, looking to refinance, or investing in a buy-to-let opportunity, we can help you understand your mortgage options so you feel confident you're making the right choice.

We also have strong relationships with private banks and other specialist lenders which may be able to provide options unavailable from the main high-street providers.

To see what we can do for you, give us a call at 0203 900 4322 or book a free consultation below.