Categories

Unlocking Savings: Is switching mortgage lenders really worth it?

Remortgaging every few years can save you thousands over your mortgage term, but new evidence suggests that more people are opting to stay with their current deal instead of exploring other options.

In a study conducted by Money Supermarket, an estimated 60% of homeowners are prepared to pay more to stay with their current lender. This may come as a surprise because, after nearly three years of high mortgage rates and an increased cost of living, many homeowners are doing what they can to keep costs down.

We all want to get the best deal possible. But, if you throw in childcare, working full-time, and potential arrangement fees on top of increased interest rates, suddenly, the labour of switching lenders to save in the long term doesn’t seem so appealing.

Is it worth the time and effort to find the cheapest deal, or should you stick with what’s easiest, even if it costs in the long term?

Related: Should You Get a Tracker or Fixed Rate Mortgage in 2024?

Why Stick With a Mortgage Lender if it’s More Expensive?

Many choose to stick with their current lenders because applying for a remortgage with a new mortgage provider involves a more stringent application process.

This could mean credit checks, application fees, and potentially a new valuation on your property. Not only is this time-consuming, but some property owners are aware of some unique challenges when remortgaging.

Valuations in particular, can present issues when remortgaging, especially in the current economic climate. In some parts of the UK, property value has dropped slightly, so if a new valuation shows that the property is valued at less than it was bought for, this can present the problem of ‘negative equity’, resulting in less favourable mortgage terms.

If your property is in negative equity, meaning its current value is less than the outstanding mortgage balance, you may even find it challenging to remortgage. Lenders typically have LTV limits, and if your property's value has decreased, your LTV ratio may exceed them, making it difficult to qualify for a new mortgage.

Additionally, you’ll likely need to pay for a solicitor, as well as any arrangement fees when switching lenders, and many Britons simply don’t have the extra cash for upfront payments like this amid the cost-of-living crisis.

For this reason, many homeowners are choosing to take the hit and wait it out with their current lenders. Staying with your current lender typically works out as the quicker, easier option.

However, convenience isn't necessarily the solution. While mortgage providers can offer preferential rates to return customers, this pales in comparison to what you could save if you switc lenders at the right time.

See similar: Are Mortgage Rates Going Down?

Is Staying with the Same Lender Right for Everyone?

No, sticking with the same lender won't be right for everyone. Unfortunately, no case has a one-size-fits-all approach when it comes to mortgages. House prices have dropped slightly in some parts of the UK, but in property hotspots like Bristol, Manchester and some parts of London, property value has increased significantly, so getting a new property valuation with a new lender can be hugely beneficial here.

Not only this, but it’s also possible to include arrangement fees in your mortgage payments, so you don’t have to pay for a new deal upfront. During your mortgage term, your credit may have improved, or you may be able to negotiate better terms now that you have built up some equity in your property.

When you take out a mortgage as a first-time buyer, you'll usually have to take the best deal offered to you. In many cases, the terms won't be favourable, and you can negotiate better rates later with a new lender. Building equity in your property means that when it's time to remortgage, you'll have a smaller loan-to-value, which can make you eligible for more attractive deals.

Sticking with your current lender might be the easy option, but getting an accurate overview of your options is important so you don’t lose out.

Working with a mortgage broker allows you to get a good overview of the deals available and what bargaining power you would have with a new mortgage provider. An experienced mortgage broker has existing relationships with lenders and can negotiate on your behalf to ensure you get the best deal possible.

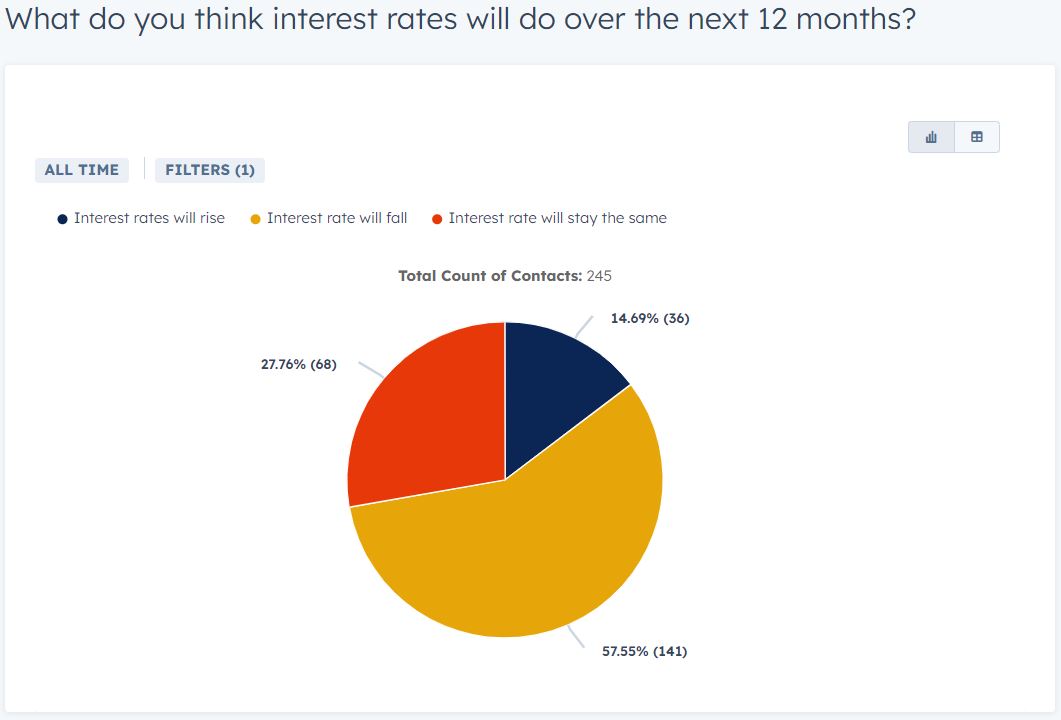

What Does the Data Say?

Our Mortgage Pulse Report shows a high level of confidence when it comes to mortgage rates. Over 85% of our audience expect mortgage interest rates to decrease or stay the same in 2024.

How to Find the Best Remortgage Option

At Clifton Private Finance, our expert advisers can offer guidance on what route to take, whether that's sticking with your current lender or taking advantage of a product with a new mortgage provider.

Our team has excellent knowledge of the market and can find you the most suitable remortgage option based on your unique financial circumstances. The process is efficient and streamlined, taking the heavy lifting out of refinancing.

Working with a professional allows you the best of both worlds. It takes the weight of researching a new deal off your shoulders and ensures you find the most cost-effective deal available.

To see what we can do for you, call us on 0203 900 4322 or book a free consultation below.