Categories

NEWS: Research Reveals Insights into UK Mortgage and Property Market in 2024

Our recent survey results provide insight into public perceptions regarding interest rates, mortgage repayments, house prices, and the housing crisis debate in the UK in 2024.

About Clifton Private Finance: Clifton Private Finance specialises in mortgage brokering and property finance, offering expert advice and solutions in the UK property finance market.

Methodology: The research was conducted through over 250 form fills on the Clifton Private Finance website, which attracts thousands of monthly visitors seeking information on property and property finance. This method ensured a diverse and relevant audience for the study.

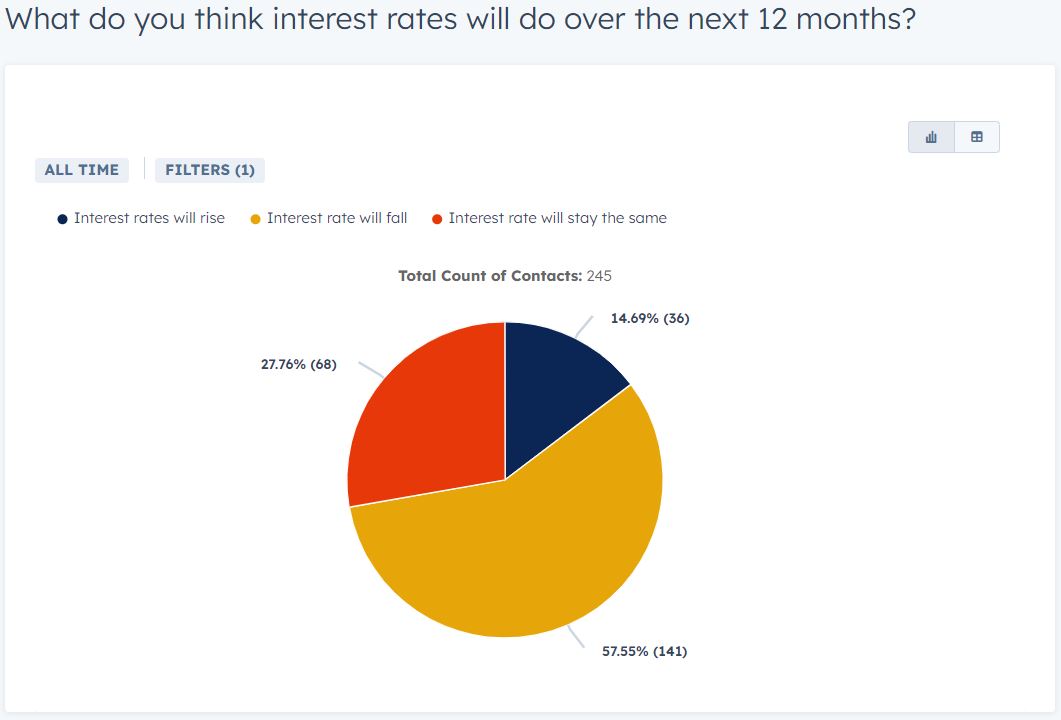

Interest Rates

- Just 15% of participants believe interest rates will rise over the next 12 months, while 85% expect either a decrease or for rates to stay the same.

This sheds some light on the fixed or tracker mortgage debate for first-time buyers and those remortgaging in the next coming months.

George Abouzolof

Senior Finance Broker CeMAP

The immediate impact of a 0.25% reduction will be a drop in mortgage payments for those on base rate trackers. Paying 0.25% less on a £1m interest-only mortgage equates to £2,500 less per year. So, the savings across the mortgage industry could be huge.

Fixed rates are unlikely to follow suit unless government bond yields relax - which they have done month-on-month. Most borrowers are opting for two-year fixes in the hope that rates will continue to drop in the future.

Relations with the US could pose a threat to the economy’s recovery. Trump is highly US-focused, and is prioritising American brands, as well as removing incentives for sustainable tech. This could make trade with US more difficult.

There are signs that US administration could go on a spending spree, which could also have a knock-on effect on us.

However, the overall sentiment has been much more neutral than we might have expected. While some landlords have been put off, for many, it’s business as usual. Investors are looking where they can to make a profit and overcome the current climate.

We’re still seeing a steady influx of first-time buyers and buy-to-lets, which could be a sign of the anticipated rush to purchase ahead of the upcoming stamp duty changes.

Furthermore, we haven’t seen a decrease in foreign investment so far, despite claims that the Autumn Budget would impact this.

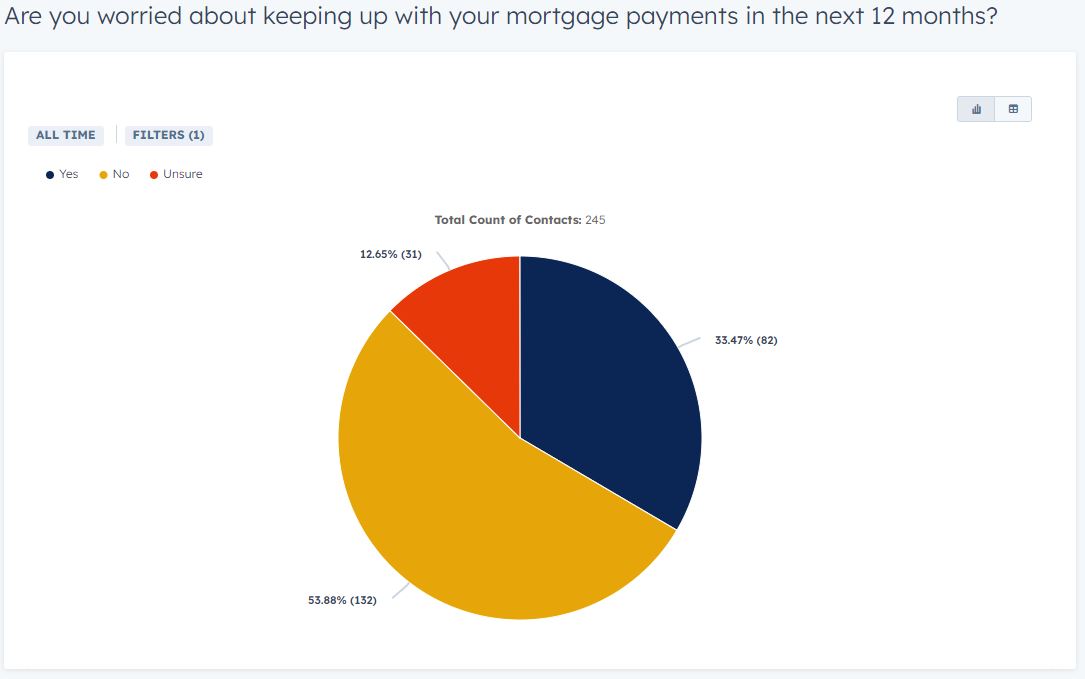

Mortgage Repayments

- Concern about meeting mortgage repayments in the next year is notable, with 33% of people worried about keeping up:

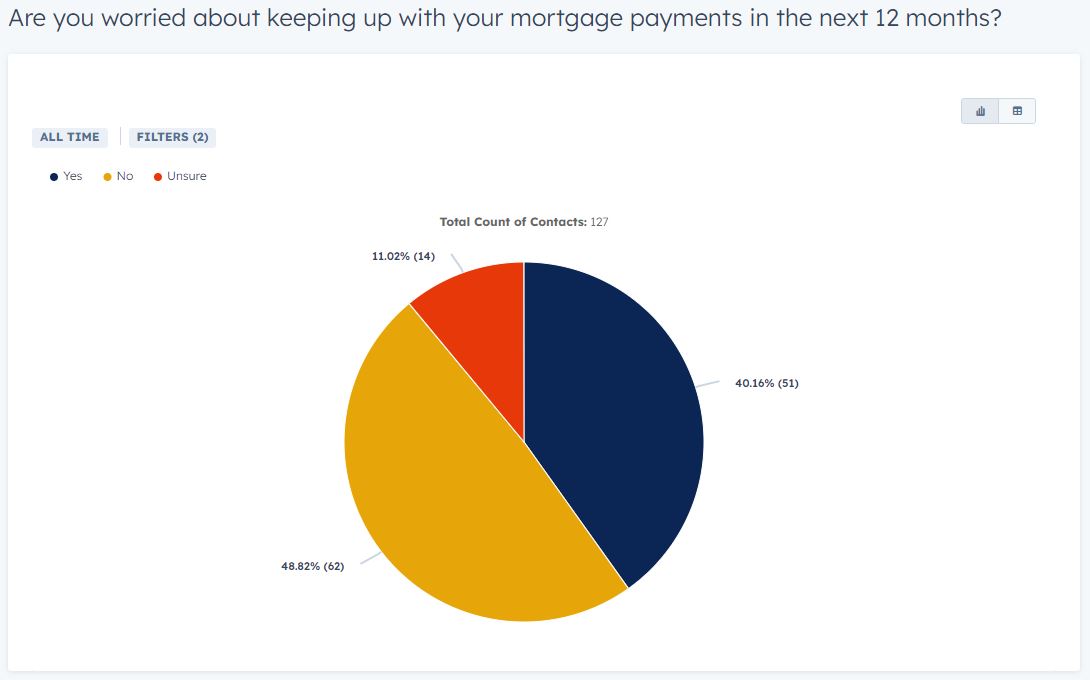

- And this increases to 40% for those earning under £50,000 per year.

Income under £50,000 per year:

George Abouzolof

Senior Finance Broker CeMAP

People are definitely worried – we see a clear concern about repayments among our clients every day.

As brokers, we look at every possible avenue to alleviate these struggles, whether it’s increasing the mortgage term, switching some or all of your mortgage to interest only, exploring offset mortgage options, and of course comparing lenders to get the most competitive deal.

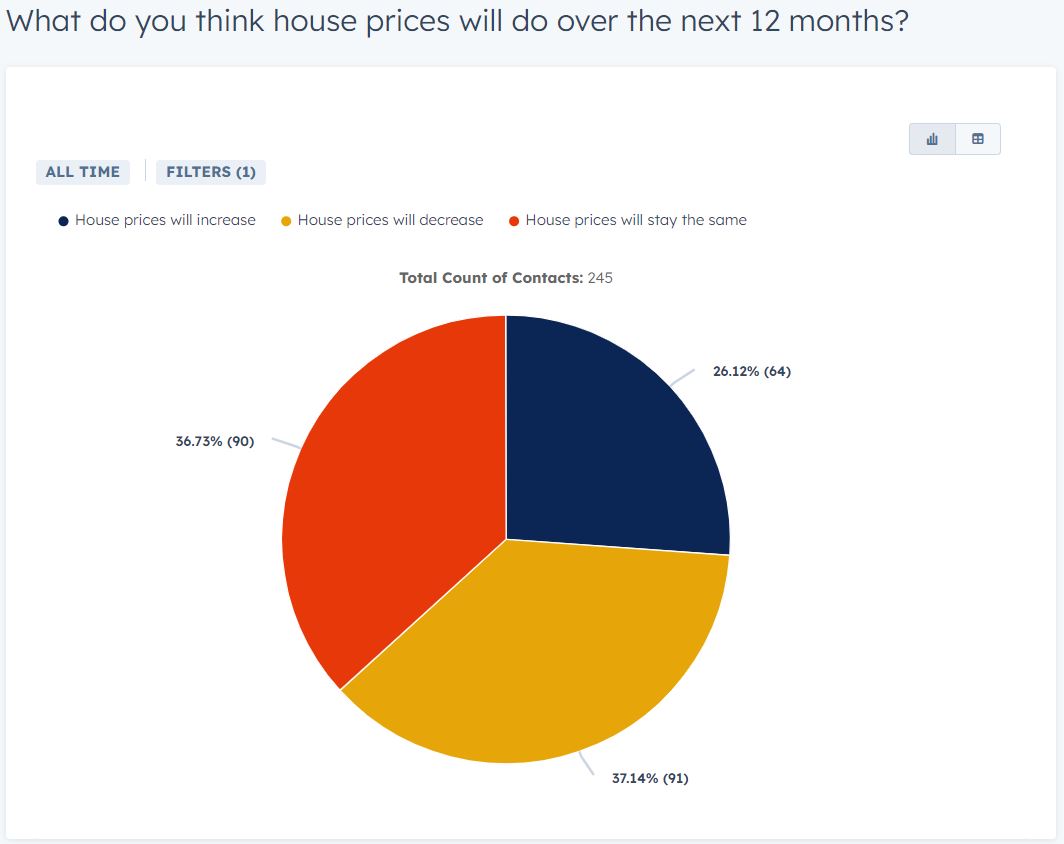

House Prices

- It’s a pessimistic outlook for property prices in the UK, with 37% of participants predicting a decrease in house prices over the next 12 months, and only 26% thinking they’ll increase.

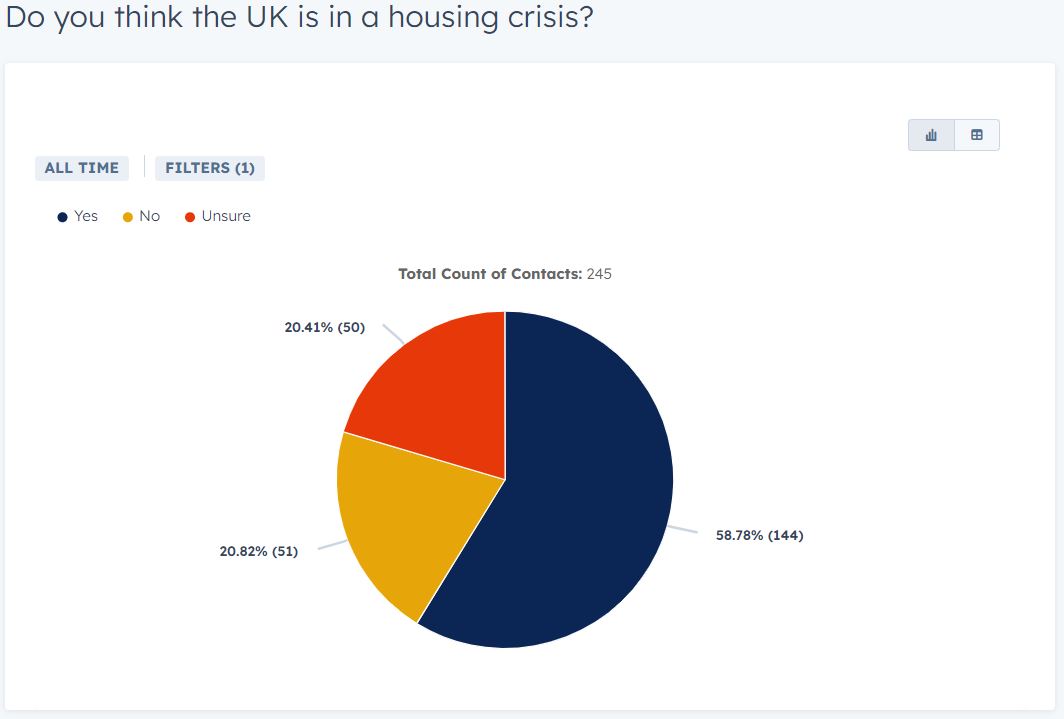

Housing Crisis:

- A significant 59% of participants believe the UK is currently facing a housing crisis.

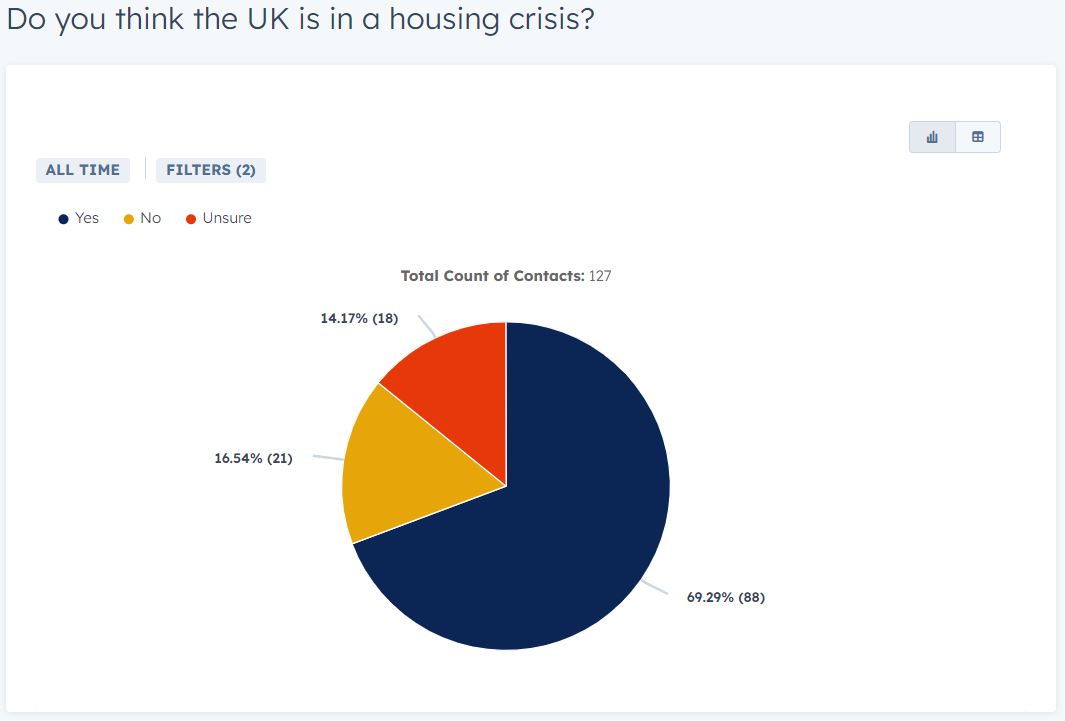

- This is more pronounced among those earning under £50k per year, with 69% affirming the crisis compared to just 46% of higher earners. It signifies a very divided outlook on housing options in the UK based on annual earnings.

Income under £50,000 per year:

For more information, please contact: sam.hodgson@cliftonf.co.uk