Mortgage Pulse Report 2024

Real Insights Into Public Opinion Of The Mortgage and Property Markets

The CPF Mortgage Pulse Report 2024 results provide insight into public perceptions regarding interest rates, bridging loans, mortgage repayments, house prices, and the housing crisis debate in the UK in 2024.

Published: 28/03/2024

Methodology: The research was conducted through over 500 form fills on the Clifton Private Finance website between November and March, which attracts thousands of monthly visitors seeking information on property and property finance. This method ensured a diverse and relevant audience for the study. Survey questions included topics surrounding mortgage rates, mortgage repayments, house price trends, the housing crisis debate, and each participant's annual income for comparative data.

The Key Findings

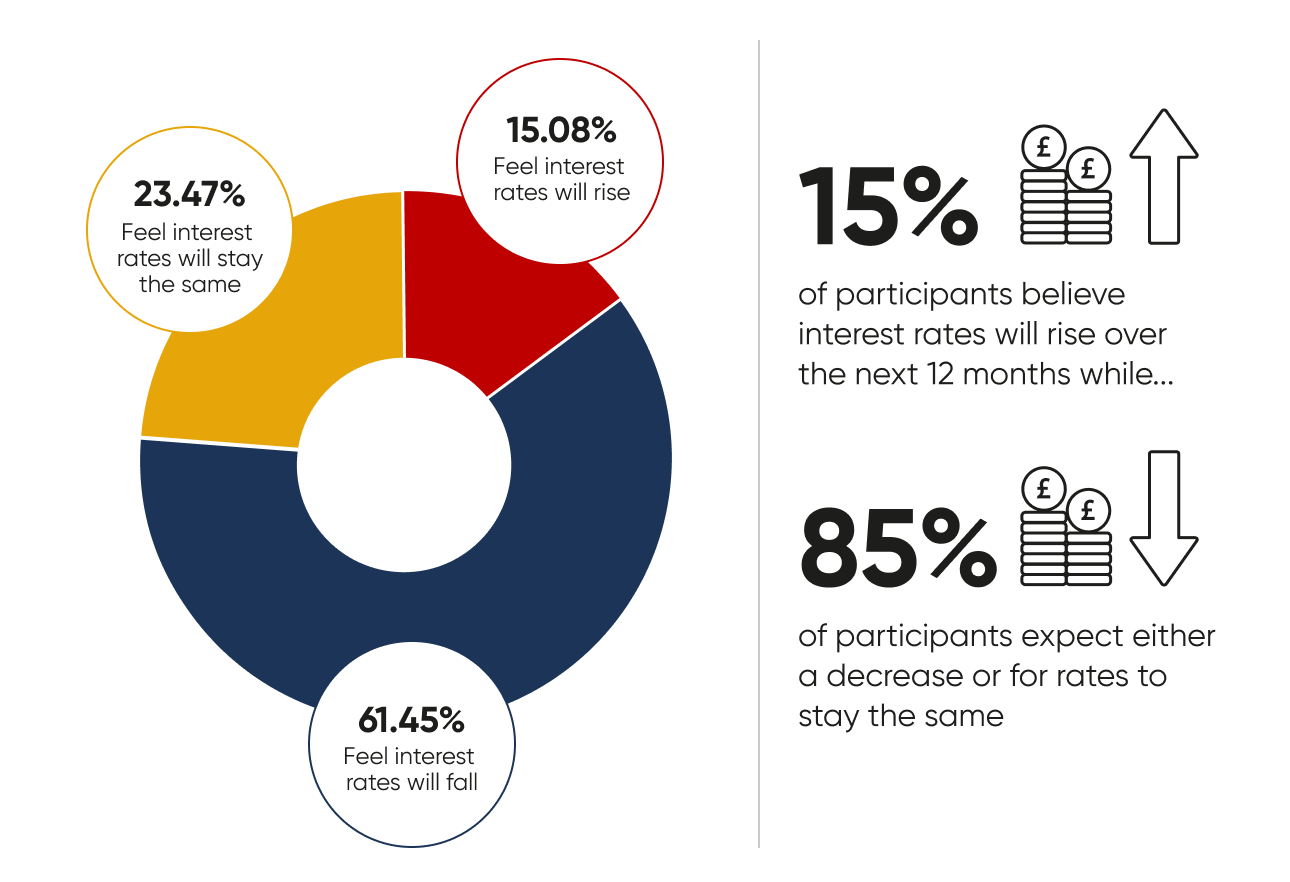

Over 85% of those surveyed don’t think interest rates will rise in 2024

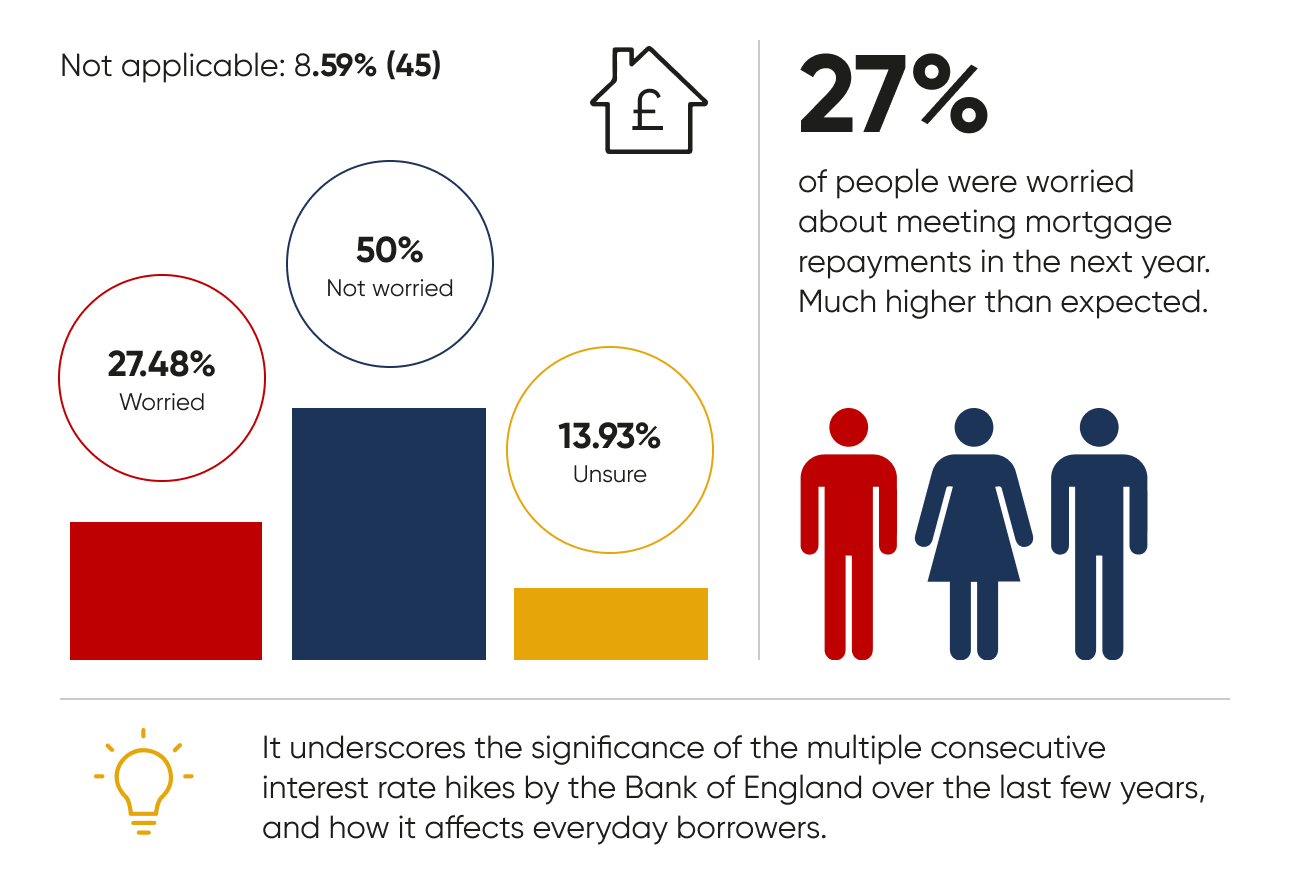

1 in 3 are worried about keeping up with their mortgage payments

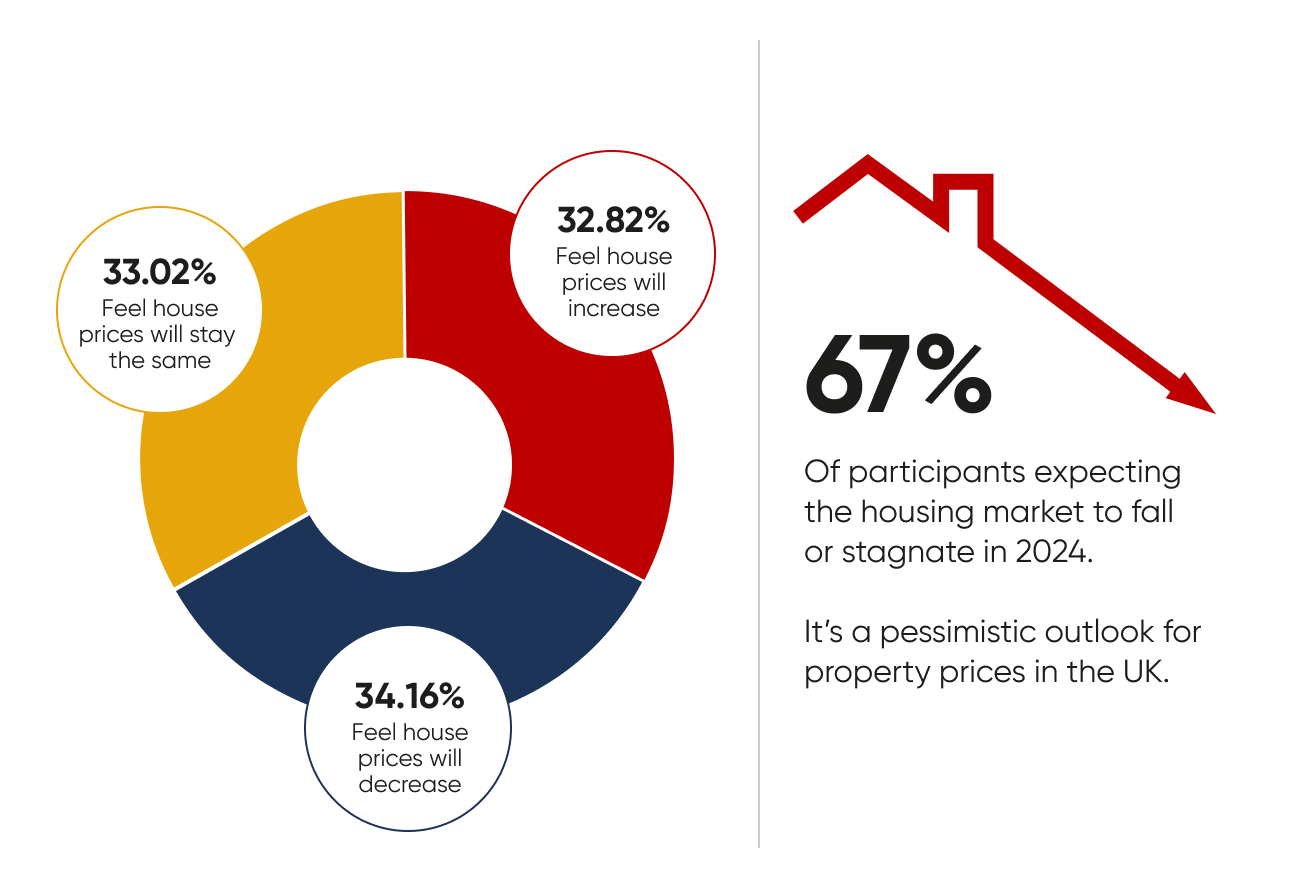

3 in 4 don’t think house prices will increase in 2024

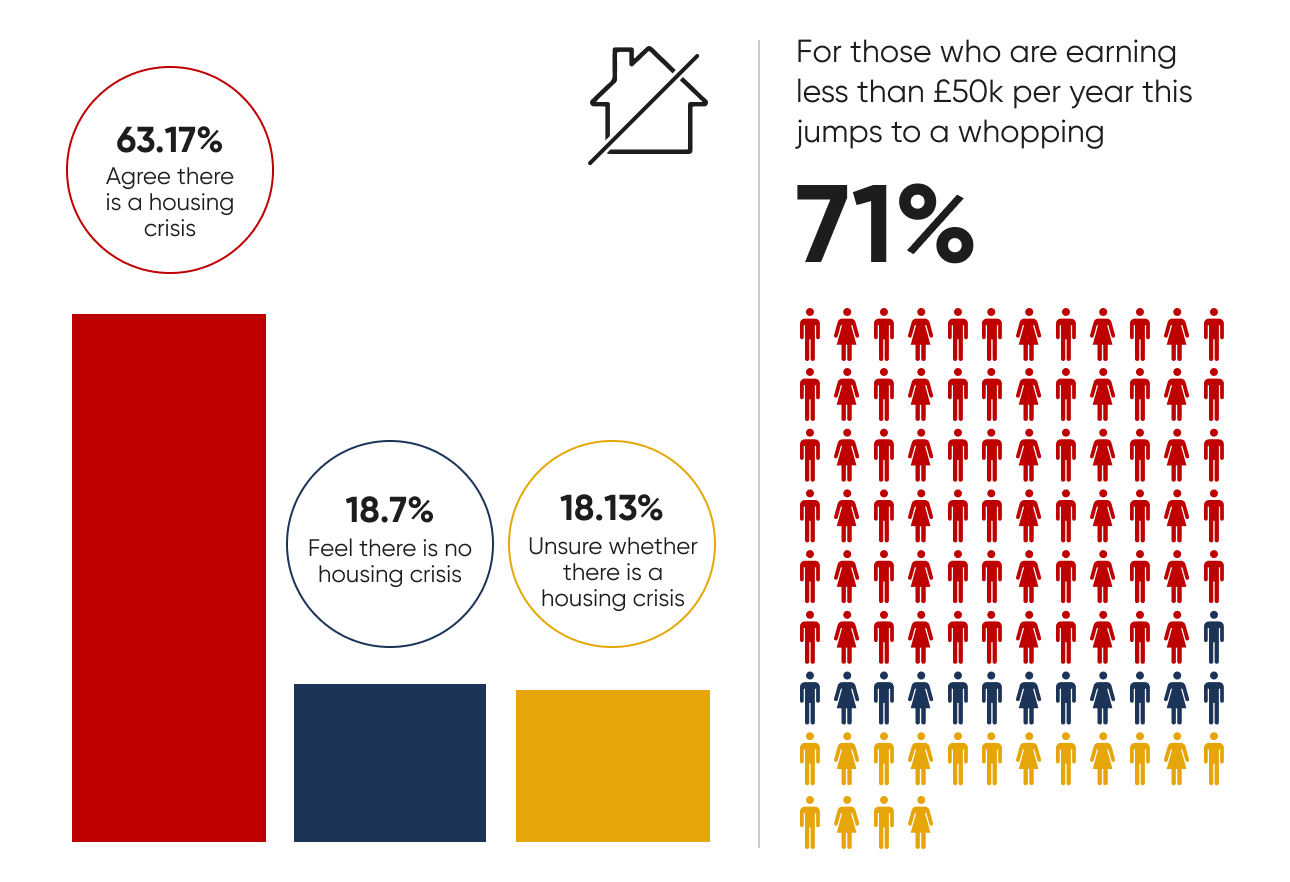

Over 60% of participants think the UK is facing a housing crisis

Over 85% of those surveyed don’t think interest rates will rise in 2024

Just 15% of participants believe interest rates will rise over the next 12 months, while 85% expect either a decrease or for rates to stay the same.

This sheds some light on the fixed or tracker mortgage debate for first-time buyers and those remortgaging in the next coming months.

George Abouzolof

Senior Finance Broker CeMAP

Whilst the BoE has kept base rates unchanged, the US Federal Reserve recently cut its rate by 0.25%, bringing it in line with the BoE. The Fed expects two more reductions this year, and if UK inflation follows a similar trend, we may do the same. A key driver could be the Autumn Budget, where tax changes might squeeze incomes, reduce spending, and ease inflation – which in theory could support lower base rates in the future.

For borrowers on tracker products, this means no immediate change to monthly payments, but sentiment in the market remains cautiously optimistic. Fixed-rate mortgages continue to edge down as swap rates and gilt yields soften, with most borrowers still opting for shorter-term fixes in the hope of future cuts.

Property investors are showing resilience, with steady activity among first-time buyers and landlords. While some are waiting for clearer signs of further rate movement, many are seizing opportunities to purchase ahead of the potential impact of Autumn Budget changes.

So far, foreign investment remains stable, reflecting wider confidence in the UK property market despite global uncertainty.

1 in 3 are worried about keeping up with their mortgage payments

Concern about meeting mortgage repayments in the next year is higher than expected, with 27% of people worried about keeping up.

It underscores the significance of the multiple consecutive interest rate hikes by the Bank of England over the last few years, and how it affects everyday borrowers.

George Abouzolof

Senior Finance Broker CeMAP

People are definitely worried – we see a clear concern about repayments among our clients every day.

As brokers, we look at every possible avenue to alleviate these struggles, whether it’s increasing the mortgage term, switching some or all of your mortgage to interest only, exploring offset mortgage options, and of course comparing lenders to get the most competitive deal.

3 in 4 don’t think house prices will increase in 2024

It’s a pessimistic outlook for property prices in the UK, with 67% of participants expecting the housing market to fall or stagnate in 2024.

George Abouzolof

Senior Finance Broker CeMAP

I always suggest looking at Nationwide's quarterly house price index for housing market insights.

The rate at which prices are falling is potentially reducing - remember, as rates drop, demand increases.

In terms of a housing crisis, there's an argument to be made that in a housing crisis, we should see house prices decreasing significantly - although we've seen drops recently, the rate of decrease is reducing, suggesting we're coming out of it.

Over 60% of participants think the UK is facing a housing crisis

It's a subjective and devising topic, but the numbers speak for themselves.

And this jumps to a whopping 71% of those who are earning less than £50k per year.

For more information, please contact: sam.hodgson@cliftonpf.co.uk