Categories

A Guide To Offset Mortgages: Are They Still A Good Idea?

With consecutive mortgage rate hikes in the UK, many homeowners are faced with huge hikes in their monthly repayments. If you are thinking of remortgaging and have savings in the bank, it may make sense to consider an offset mortgage - a lesser-known product that could help you save money on your repayments.

Anyone with a considerable amount of savings may be well served by an offset mortgage, which can result in lower monthly payments and even allow you to pay off your mortgage more quickly.

Yes, mortgage rates are up - but savings rates are up too, so tying your mortgage and savings together can make your repayments more manageable and potentially save you money in tax in the long run.

Here we explore the advantages of offset mortgages in the current economic environment, what to consider before applying, and the circumstances where it could save you money (particularly important for higher and additional rate tax payers will large savings accounts!).

And if you'd like to speak to an adviser about whether they're right for you and your mortgage - you can book a free consultation with us.

In this guide:

How do you work out if it's worth it for you?

Can I Still Withdraw My Savings?

Can I Use Any Savings Account for an Offset Mortgage?

Are Offset Mortgages a Good Idea?

What Types of Offset Mortgages Are Available?

How Much Can I Actually Save with an Offset Mortgage?

Can I Offset My Mortgage Manually?

Can I Get an Offset Mortgage if I'm Self Employed?

Can I Get a Large Offset Mortgage Loan?

How Can I Get the Best Offset Mortgage?

What is an Offset Mortgage?

An offset mortgage links your mortgage to your savings account.

Your savings are effectively 'offset' against your mortgage balance, thereby 'reducing' your mortgage, so you pay less interest on a smaller debt.

For example, you have £100k in savings and a £200k mortgage - an offset mortgage effectively reduces your debt to £100k, meaning your monthly repayments are lower.

While traditionally you can either use your savings to:

- Help pay for your monthly mortgage repayments manually, by simply allocating the interest you earn to your mortgage repayment budget.

- Or pay off a chunk of your mortgage to reduce your debt, meaning you pay interest on a smaller balance and reducing your monthly repayments.

The problem with these two methods is that:

- a) Earning interest on a savings account is subject to income tax depending on your income tax bracket and the amount you have in savings.

- b) Once you pay off a chunk of your mortgage, you can't get that equity back - there's no flexibility.

This is where offset mortgages come in.

By linking your savings account to your mortgage, you can earn interest without worrying about paying tax on it, as it's simply reduced from your mortgage balance instead.

And, your savings account isn't locked away forever - you can still dip into your savings account and switch to a standard mortgage if you wish at any time.

Check out our case study below, and read on for more examples and a breakdown of how the tax works on savings accounts.

How Do Offset Mortgages Work?

The more savings you have, the more you can reduce your mortgage balance - most lenders allow you to offset up to 100% of your mortgage if you have the savings in place, meaning you'll pay zero interest. Certainly an attractive deal considering the interest rates on mortgages currently.

However, you need to keep in mind the tax on savings interest that could eat into this £5,000 from your savings account, depending on your income bracket.

Here is a table that simplifies how interest is taxed in the UK based on your income tax bracket:

UK Tax on Interest Income

| Tax Allowance | Description | Dependence on Income Tax Band | Example(s) |

| Personal Allowance | Up to £12,570 you can earn tax-free. Applies to wages, pension, or other income first. | None | If you earn £16,000, the first £12,570 is tax-free. |

| Starting Rate for Savings | Up to £5,000 of interest is tax-free. | Income up to £17,570 | If you earn £16,000 and use up £12,570 as personal allowance, you can still earn up to £1,570 (£5,000 - £3,430) interest tax-free. |

| Personal Savings Allowance | Additional interest income that can be earned tax-free. | Based on Income Tax Band | Basic rate: £1,000, Higher rate: £500, Additional rate: £0 |

Summary:

So, how do you work out if an offset mortgage is worth it for you?

You need to work out if you're paying tax on the interest in your savings account, and if so whether avoiding this tax via an offset mortgage would be worth it (it still might not be if you could get a much better savings account rate elsewhere and offset this manually).

Step 1: Calculate the net annual interest you'd earn from your savings if you held them in the best instant-access* savings account on the market.

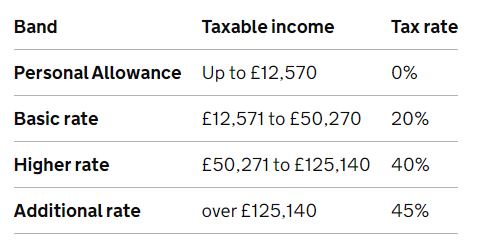

To get your net interest earnings, deduct income tax relative to the amount that would be taxable based on your earnings (see the above table) and the tax rate you'd pay (e.g., 0%, 20%, 40% or 45%). Here are the current income tax rates in the UK as a reminder:

Step 2: Next, look at the best standard mortgage deal on the market for your preferences (e.g., 5-year fixed rate), and subtract your net annual interest from your mortgage payments - how much have you saved? Make a note of your net monthly repayment figure.

Step 3: Finally, compare this to the best offset mortgage product on the market (we can find this for you if you're unsure). If your repayments with an offset mortgage are cheaper than the net repayments you had earlier, then an offset mortgage will save you money. Remember to check your calculations with a qualified tax advisor.

*We've mentioned instant access savings accounts for the comparison simply because you have instant access to your savings with an offset mortgage, so it's a like-for-like comparison. However, there may be fixed-rate savings products with more attractive interest rates, albeit with less flexibility.

It's important to note that while most do, not all lenders will allow you to offset 100% of your savings balance, and this will affect your calculations.

Read blog: How to Get a Large Mortgage with Multiple Income Sources

Case study: Read our case study below on how we raised over £650k on an offset mortgage for a London barrister buying a second home in Somerset

Can I Still Access My Savings?

Yes, you can access the savings account linked to your offset mortgage loan whenever you want. This is one of the great advantages because it's easier and cheaper to get your money back than remortgaging to release equity.

However, if you do draw down on your savings account, it will reduce the amount you can offset against your mortgage loan, so your monthly payments will go up. You should also bear in mind that some lenders may require you to keep a minimum amount in your savings account.

Can I Use Any Savings Account for an Offset Mortgage?

No, if you take out an offset mortgage, the lender will offer you a savings account linked to your mortgage.

Whether or not the interest rates offered with your offset mortgage savings account will reflect the current market will depend on the lender.

It’s important to note that the savings you can make through your offset mortgage depend entirely on the amount of savings you have in that account and the interest rates you have arranged with your lender.

A specialist mortgage broker will have in-depth knowledge of the market and can find the best deals on your behalf.

At Clifton Private Finance, we have long-term relationships with mainstream and private lenders, and we can find deals with specialist banks that you otherwise may not have access to.

Call us on 0117 959 5094 or click here to make an online enquiry with us.

Are Offset Mortgages a Good Idea?

It's always best to speak to an independent mortgage broker to get expert advice when deciding on a new mortgage product. A mortgage broker can help you decide whether an offset mortgage will be the best option, weighing up the pros and cons or whether there might be a better mortgage product to suit your circumstances.

Advantages

- An offset mortgage can be an excellent way to make your savings work harder for you

- Adding your current account can lead to further savings (a small number of lenders allow you to do this)

- You’ll pay off your mortgage more quickly or benefit from lower monthly repayments

- You can still access your savings easily if the need arises, giving you more flexibility

- Most lenders let you make overpayments on your offset mortgage which also reduces the amount of interest you are charged

- You won't pay tax on the savings you make on interest charges

- If you're self employed or a contract worker, you can use the savings you make on interest payments to save up for your annual tax bill

- You can link your savings account to a family member's mortgage (otherwise known as a family offset mortgage). This is a great way to help a first time buyer get on to the property ladder.

What to Consider

- Offset mortgages do come with more expensive interest rates compared to other mortgage products

- You won't earn any interest on the savings you have in your offset account

- Paying a larger deposit in the first place to lower your Loan To Value (LTV) could make more sense, giving you access to lower rates and interest payments - although your savings will be locked in

What Types of Offset Mortgages Are Available?

Offset mortgages can come in various forms, each type offering different levels of flexibility and potential cost savings for homeowners.

There is a range of offset mortgage loans available:

- Fixed-rate offset mortgage - The interest rate you pay on the mortgage after it has been linked to your savings account is fixed for a set term – usually two, three or five years, although some lenders will go to 10 years.

- Tracker offset mortgage - The interest rate you pay on your offset mortgage is variable and follows the Bank of England base rate.

- Discount offset mortgage - The interest rate you pay on your offset mortgage is given a set discount on the lender’s standard variable rate (SVR)

- Interest Only offset mortgage - As with a standard interest only mortgage, you only pay interest on the loan and this will depend on how much of your mortgage is offset by your savings.

- Family offset mortgage - You can link your own savings account to a child or grandchild's mortgage, helping them to pass lender affordability criteria and reducing their interest payments.

Each type of offset mortgage comes with its own benefits and considerations. Factors like interest rates, terms, and any associated fees should be carefully evaluated based on your financial goals and circumstances.

Speaking with a specialist mortgage broker can help you determine which type of offset mortgage aligns best with your needs and can also get you the best deal on the market for your specific circumstances.

Speak to one of our specialist mortgage advisors today to discuss your situation and find out which offset mortgage product might suit you best.

How Much Can I Actually Save with an Offset Mortgage?

One of the main advantages of an offset mortgage is that you can put the interest you generate on your savings account towards your mortgage interest.

This means if you have a large amount of savings, if you are a high earner, or have inherited a large amount of money, for example, an offset mortgage could be a convenient option.

Convenience is key here, as while it is very much possible to save with an offset mortgage, potentially more so than with a standard mortgage, it’s not necessarily the most efficient way to save in every scenario.

You may not be able to offset 100% of your savings against your mortgage interest, and you may be able to find savings accounts with other lenders that offer you better interest rates.

This means that if you were to open a separate savings account with a higher interest rate and put the interest you generate on that money towards paying your mortgage interest, you may be able to save more.

While this option doesn’t technically count as ‘offsetting’, it does offer a similar result, with more flexibility compared to some offset mortgage deals.

However, you would potentially need to pay tax on this interest as we covered earlier, so again it depends on your situation and the deals available at the time. If you're unsure, speak to one of our advisers about your situation and plans.

Watch our video below to find out how our clients raised £1M capital with an interest-free offset mortgage:

Can I ‘Offset’ My Mortgage Manually?

If your priority is getting the most out of your savings, but an offset mortgage isn’t for you, it is possible to take out a separate savings account and put the interest towards your mortgage manually.

This method could allow you to save more overall, but it does require more admin than with an offset mortgage, which is automatic, and you could also be subject to income tax on the interest you earn as we've discussed.

While manually putting your savings interest towards your mortgage doesn’t technically count as an ‘offset mortgage’, it may allow you to achieve a similar result.

You can use online savings comparison tools such as Simply Savings Accounts, which lists the best savings accounts on the market, their eligibility criteria, and individual benefits.

- However, it is important to note that because you are paying your mortgage interest manually, it’s likely that your interest payment dates will not coordinate with your mortgage interest payments.

- Interest on savings accounts is typically paid monthly in the UK, but for some accounts, it can be deposited quarterly or even annually.

- And even if you do choose a savings account where the interest is paid monthly, you may still have to pay your mortgage interest before you get paid interest on your savings.

It’s advisable to weigh up whether this is manageable for you and if you’re prepared to pay your savings interest towards your mortgage in arrears.

Our team of brokers can guide you through the application process and connect you with lenders who can accommodate more complex income structures and offer tailored financial solutions.

Can I Get an Offset Mortgage if I'm Self-Employed?

It is possible to get an offset mortgage if you’re self-employed or working as a contractor. This option would typically be available through a specialist lender.

Lenders will apply different affordability criteria and want to see 3 years of accounts and, potentially, proof of future earnings.

If you're self-employed, an experienced mortgage advisor can talk you through the process of applying for a mortgage and connect you to a specialist lender who can accommodate this type of offset mortgage application.

Can I Get a Large Offset Mortgage Loan?

Yes, there are a number of specialist lenders willing to grant large offset mortgage loan applications. Affordability criteria can be stricter, and you may need to put down a larger deposit.

However, we have helped many clients borrow over one million pounds with an offset mortgage loan.

See similar: How to Get a Multi-Million Pound Mortgage

How Can I Get the Best Offset Mortgage?

At Clifton Private Finance, our expertise and knowledge of the mortgage market mean we can match you to the best mortgage product and lender to suit your circumstances. If you're looking to further explore your options, you may find it helpful to speak to one of our specialist mortgage advisors.

We have close relationships with high street banks and specialist lenders offering the best offset mortgage rates and terms. We can guide you through the application process, negotiate on your behalf, and find funding solutions tailored to your needs.

Call us on 0203 900 4322 to discuss your requirements.Or you can book a free consultation with one of our expert advisors at a convenient time for you below.